Key Messages

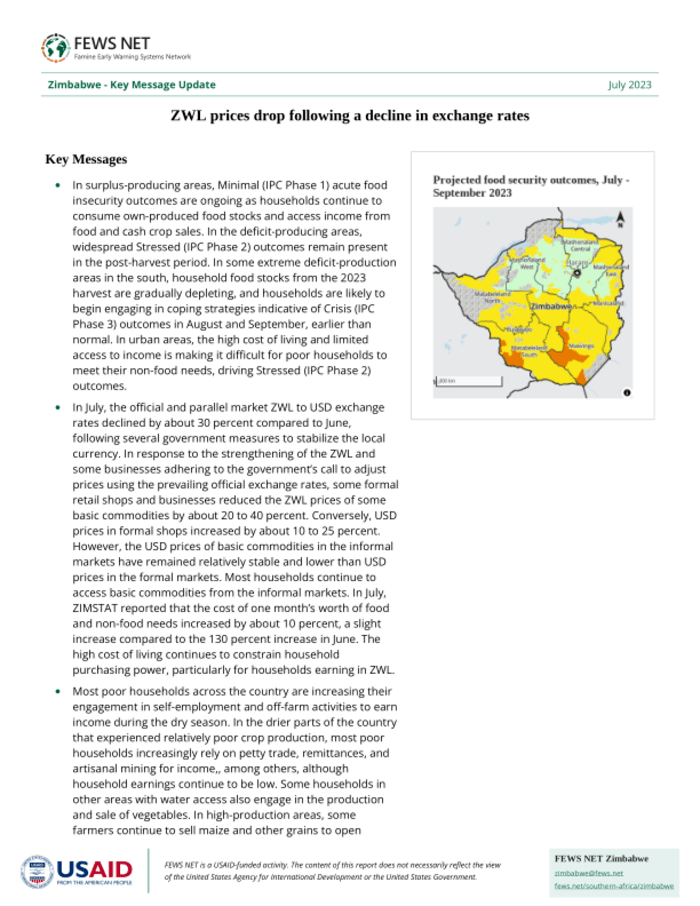

- In surplus-producing areas, Minimal (IPC Phase 1) acute food insecurity outcomes are ongoing as households continue to consume own-produced food stocks and access income from food and cash crop sales. In the deficit-producing areas, widespread Stressed (IPC Phase 2) outcomes remain present in the post-harvest period. In some extreme deficit-production areas in the south, household food stocks from the 2023 harvest are gradually depleting, and households are likely to begin engaging in coping strategies indicative of Crisis (IPC Phase 3) outcomes in August and September, earlier than normal. In urban areas, the high cost of living and limited access to income is making it difficult for poor households to meet their non-food needs, driving Stressed (IPC Phase 2) outcomes.

- In July, the official and parallel market ZWL to USD exchange rates declined by about 30 percent compared to June, following several government measures to stabilize the local currency. In response to the strengthening of the ZWL and some businesses adhering to the government’s call to adjust prices using the prevailing official exchange rates, some formal retail shops and businesses reduced the ZWL prices of some basic commodities by about 20 to 40 percent. Conversely, USD prices in formal shops increased by about 10 to 25 percent. However, the USD prices of basic commodities in the informal markets have remained relatively stable and lower than USD prices in the formal markets. Most households continue to access basic commodities from the informal markets. In July, ZIMSTAT reported that the cost of one month’s worth of food and non-food needs increased by about 10 percent, a slight increase compared to the 130 percent increase in June. The high cost of living continues to constrain household purchasing power, particularly for households earning in ZWL.

- Most poor households across the country are increasing their engagement in self-employment and off-farm activities to earn income during the dry season. In the drier parts of the country that experienced relatively poor crop production, most poor households increasingly rely on petty trade, remittances, and artisanal mining for income, among others, although household earnings continue to be low. Some households in other areas with water access also engage in the production and sale of vegetables. In high-production areas, some farmers continue to sell maize and other grains to open markets and the Grain Marketing Board (GMB), with the supply of maize onto the open markets expected through early 2024, especially in surplus-producing areas. As of early July, tobacco and cotton sales were more than 50 and 400 percent higher than last year, respectively, thereby contributing to improved access to income for some households in the tobacco and cotton growing areas.

- Livestock prices are declining earlier than normal in some drier parts of the country as pasture availability, water access, and livestock body conditions deteriorate in the dry winter season. However, livestock conditions in other parts of the country, including high rainfall areas, are in fair to good condition, and prices remain stable, although pasture conditions are also seasonally deteriorating. There is increasing concern that an erratic start to the 2023/24 rainy season due to El Nino will limit the regeneration of pasture and water resources and the recovery of livestock body conditions, particularly in the drier southern and western areas of Zimbabwe.